The "rich get richer" headlines are real — but watching that scoreboard pays you nothing, and the wealth tax everyone's fighting about would barely touch your life. Two numbers decide whether you're broke: what you earn, and what you keep after taxes. Here's that story, by the numbers, without the outrage.

The receipts are real

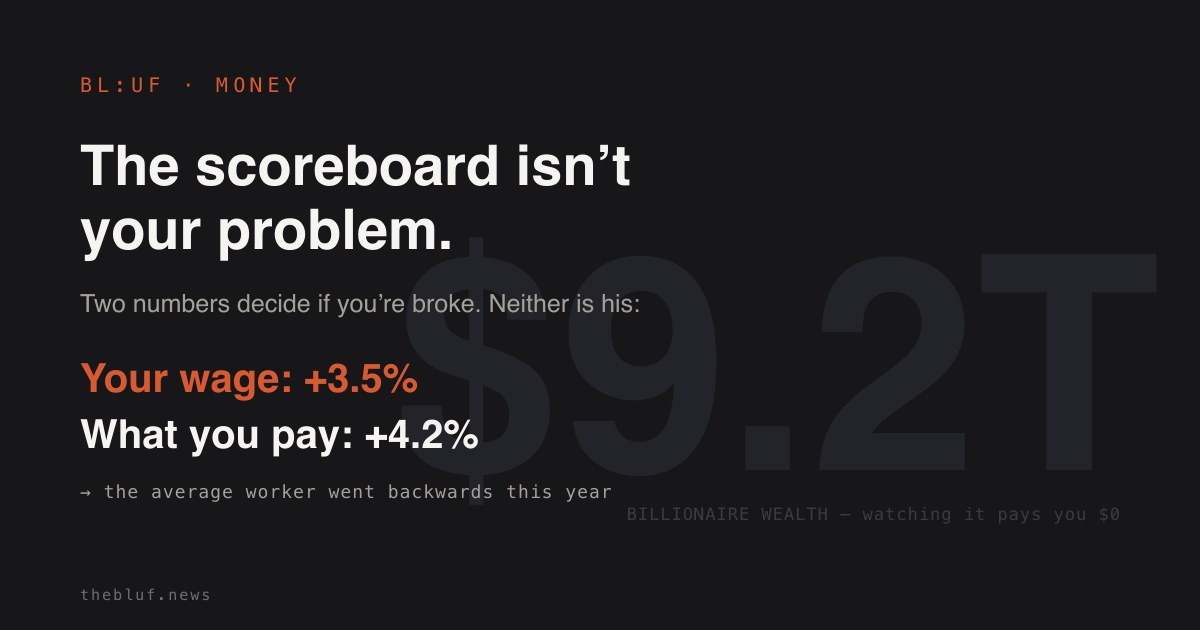

US billionaires are worth about $9.2 trillion, up roughly a third in one year (Americans for Tax Fairness, June 2026). Workers' share of the economy — the slice of everything the country produces that goes to wages — fell to 53.8%, the lowest since the government started counting in 1947 (Bureau of Labor Statistics). In June, Elon Musk became the first person ever worth $1 trillion. Those numbers are accurate. The question is what they have to do with you.

Almost nothing — and that's the part the outrage genre buries

Musk's net worth has roughly zero pull on your rent. The number that runs your life is smaller and closer: your hourly pay against the cost of food and housing. This year that gap moved the wrong way — prices rose 4.2% while the typical worker's pay grew about 3.5% (BLS CPI and the Atlanta Fed, May 2026), so the average worker went backwards. 66 million Americans — about 45% of workers — make under $25 an hour (Economic Policy Institute). Credit-card debt hit a record $1.28 trillion (New York Fed, Q4 2025). That's the problem. Not the scoreboard.

### Where to get that proof — free

A skill that moves your pay is one you can prove — a credential an employer recognizes, or a foot inside a real company. A few programs that actually deliver that, free or nearly, each with its catch:

- Per Scholas — 100% free tech training, certification exams included, wired into 850+ employer partners. Income-qualified, full-time. (perscholas.org)

- Year Up United — free and pays a stipend; ages 18–29, includes an internship at a real company. (yearup.org)

- Verizon Skill Forward — free edX certificates, no Verizon account needed; just be 17+ and in the US. (register.edx.org/verizon)

- Google Career Certificates — employer-recognized; about $49/month on Coursera unless you take the financial aid or a partner scholarship — do that first. (grow.google/certificates)

- Amazon Career Choice — prepaid tuition up to $5,250 a year, but you have to be an Amazon employee. (amazon.com/careerchoice)

Pick the one whose catch you can clear, and finish it.

The billionaire tax won't fix it either

Take California's proposal — a 1.5% yearly tax on fortunes over $1 billion. Best case, if the state collected the whole thing and mailed it in equal checks to all 39 million Californians, that's roughly $32 to $42 a month per person. And it won't be — the money funds programs, not your bank account. It does nothing to your hourly wage. It's aimed at the top; it doesn't reach down to you.

So why do billionaires spend millions fighting it? Arithmetic, not cartoon villainy

A wealth tax hits everything you own, every year — not just what you earned this year. Someone worth $50 billion, taxed 1.5%, owes $750 million a year, forever, even in a year they earn nothing. Spending $30 million on ads to kill that tax saves $750 million a year — it pays for itself in weeks. Anyone would take that bet. The deeper fear isn't the cash: to pay a tax on stock they haven't sold, founders have to sell shares — and sell enough, and they lose control of their own company.

The story nobody's selling you: you're taxed harder for working than for owning

The same dollar is taxed differently depending on how you got it. A paycheck — "ordinary income" — is taxed up to 37%. Money you make because something you own went up and you sold it after a year — a "long-term capital gain" — is taxed at 0, 15, or 20% (IRS). Working money is taxed harder than owning money. That's not a glitch; it's written into the code.

And the very top can sidestep even that, legally — call it Buy, Borrow, Die:

- Buy stock and never sell it. Selling is what triggers the tax; if you don't sell, there's no "income."

- Borrow against it to live on. A loan isn't income, so it isn't taxed.

- Die, and a rule called step-up in basis wipes most of the built-up gains for your heirs. (Estates above $15 million still owe estate tax — but the income tax on decades of growth largely vanishes.)

Two more quiet ones: the Social Security tax stops at $176,100 of income (2025) — so it takes a bigger percentage bite out of a $50,000 worker than a millionaire — and carried interest lets fund managers pay the lower "owning" rate on what is really their pay.

The honest other side

Because it's real: the lower rate on owning is deliberate — it's meant to push people to invest in companies that create jobs. About 6 in 10 Americans own some stock, mostly through retirement accounts, so a rising market reaches past the billionaires too. And taxing wealth a person hasn't sold yet is genuinely hard to do fairly. You don't have to pick a side to see the machine clearly.

Where your leverage actually is

Not the scoreboard — these:

- Your wage. The biggest mover of your number is what you earn an hour: switching jobs (still the fastest raise most people get), a skill or credential an employer can actually verify, and the minimum-wage laws you vote on locally.

- The owner's break you're allowed to claim. The tax code hands owners a discount — and lets regular people grab a slice of it through tax-advantaged accounts: a 401(k) or IRA, and an HSA if you qualify. Same lower-tax treatment the wealthy use on "owning money," opened to you on purpose.

The billionaire's number will keep going up, and the headlines will keep selling you the anger for free. Your wage and what the tax code lets you keep — those you can actually move.

Sources: BLS (labor share, CPI), Atlanta Fed Wage Growth Tracker, Economic Policy Institute, NY Fed Household Debt & Credit Report, Americans for Tax Fairness, IRS (Topic 409, §1014, estate exemption), SSA (wage base).